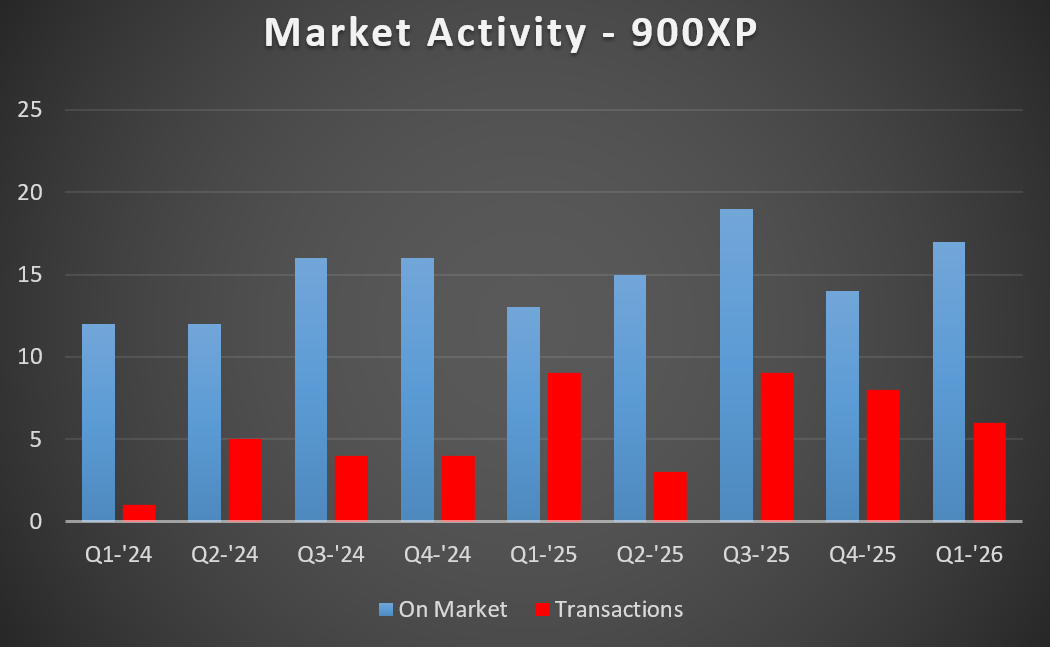

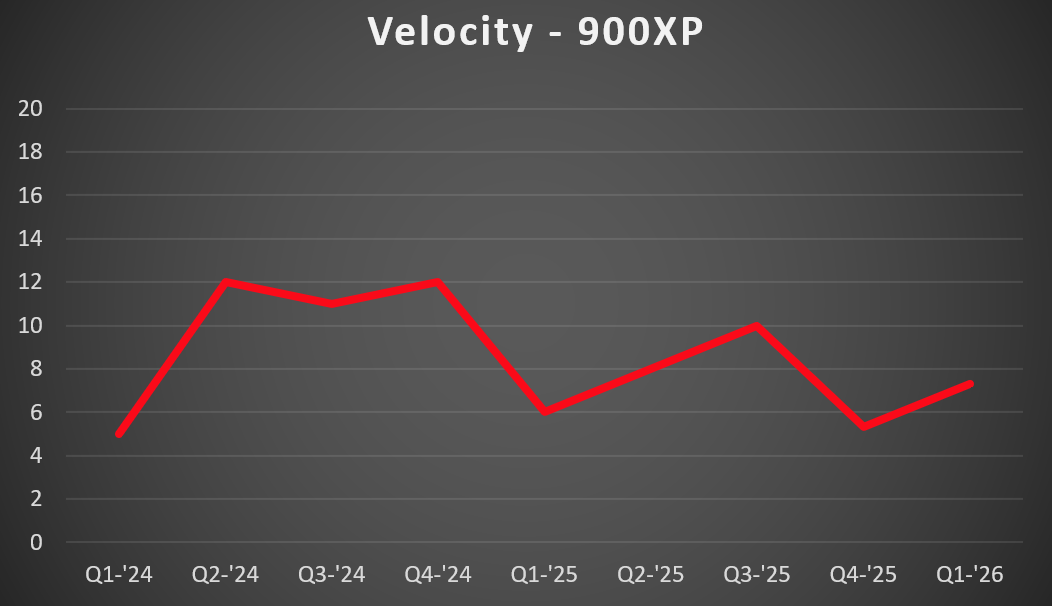

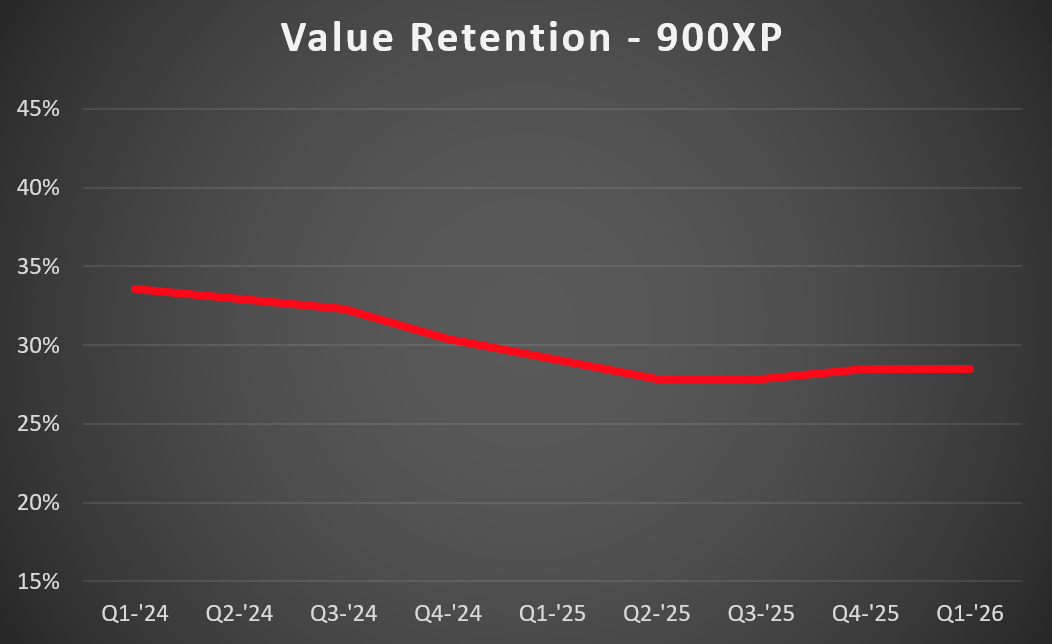

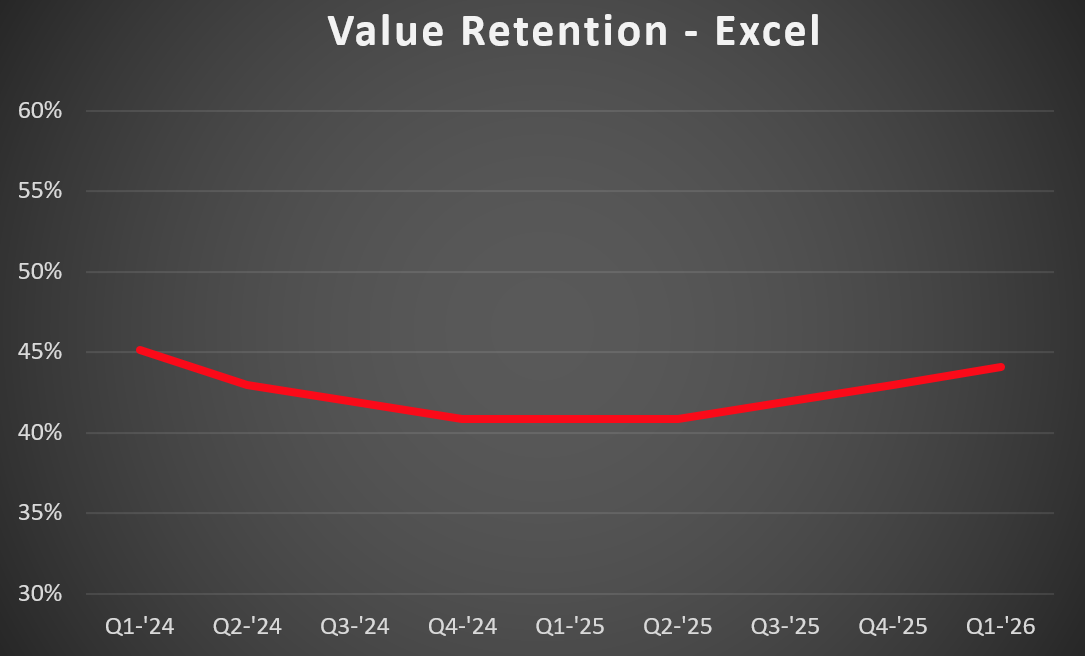

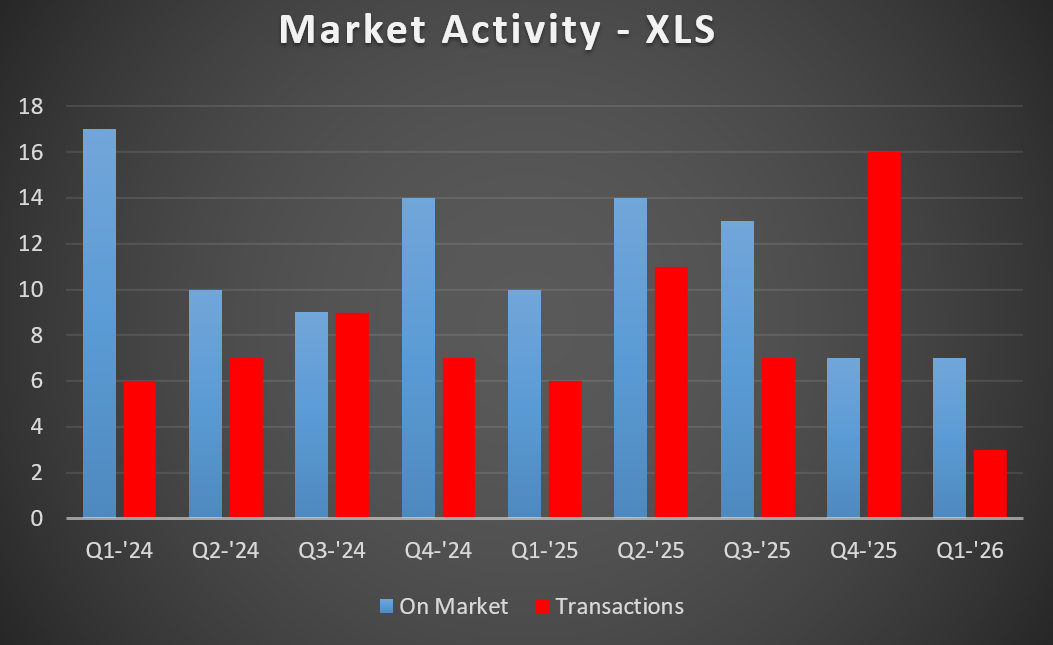

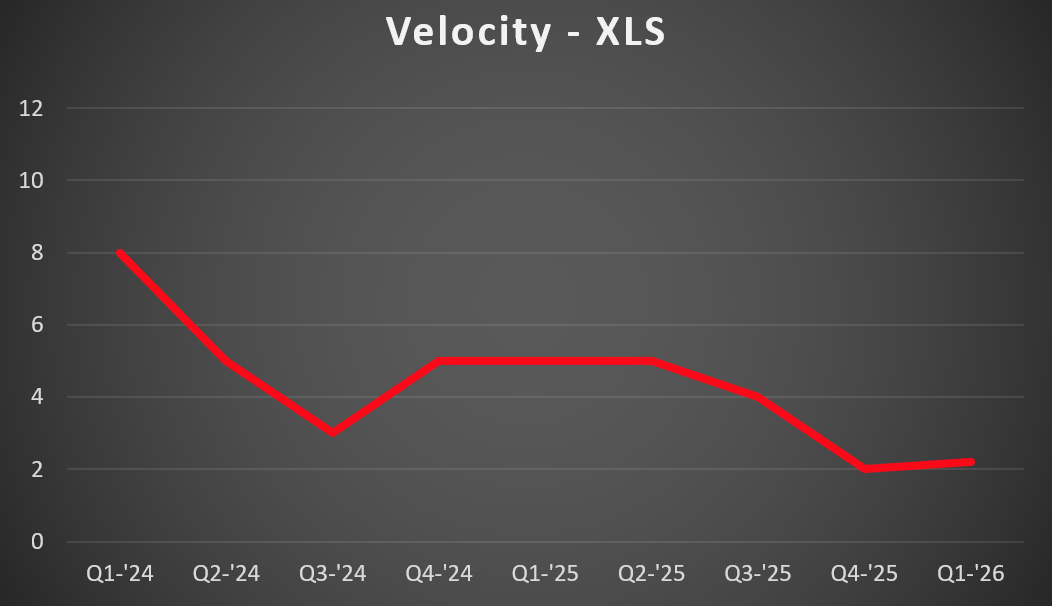

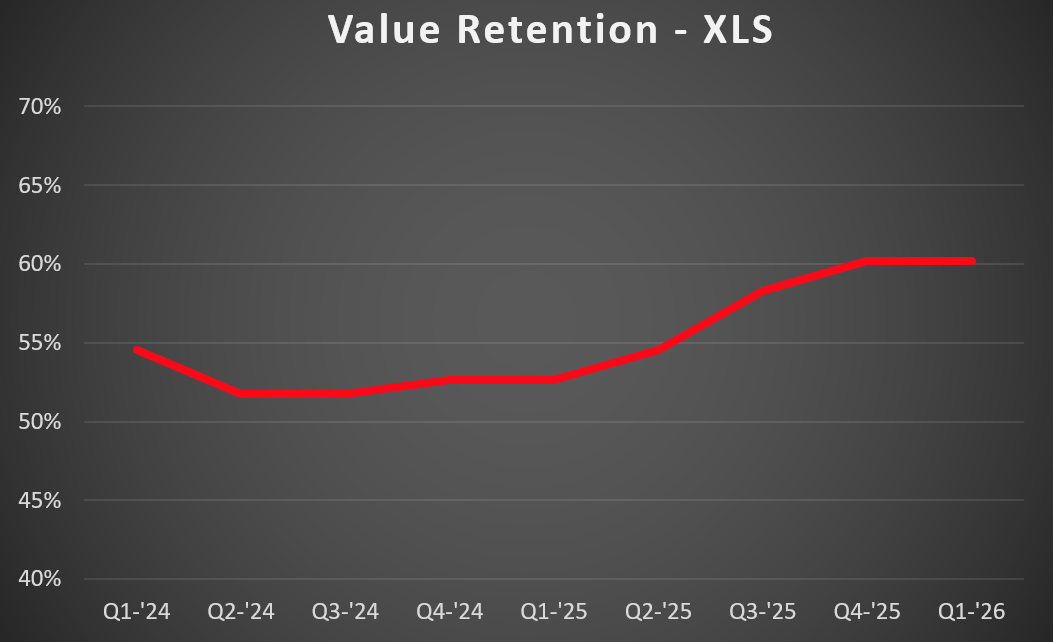

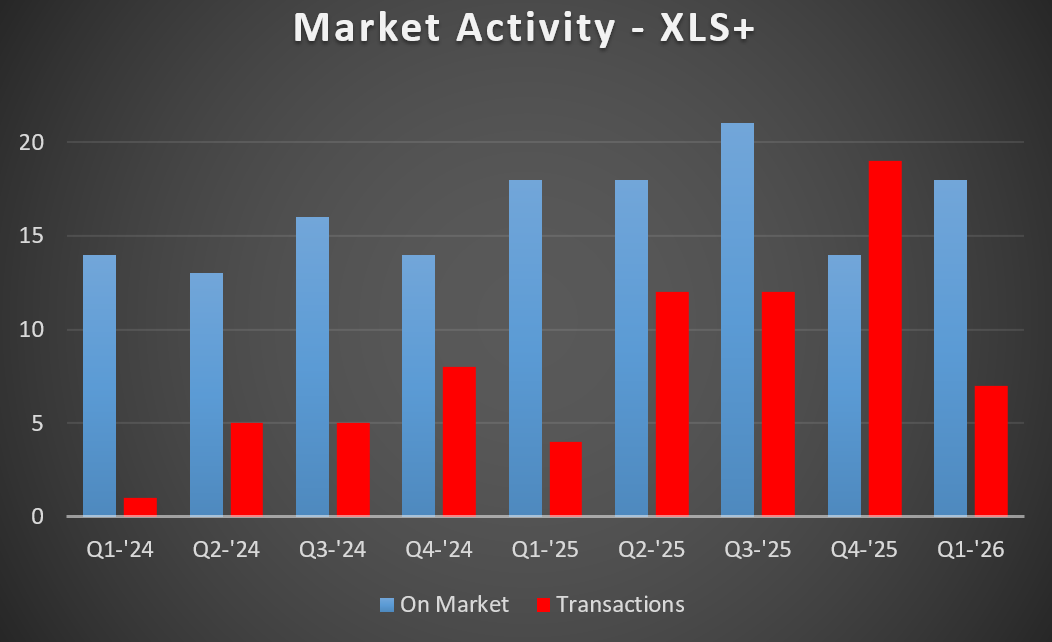

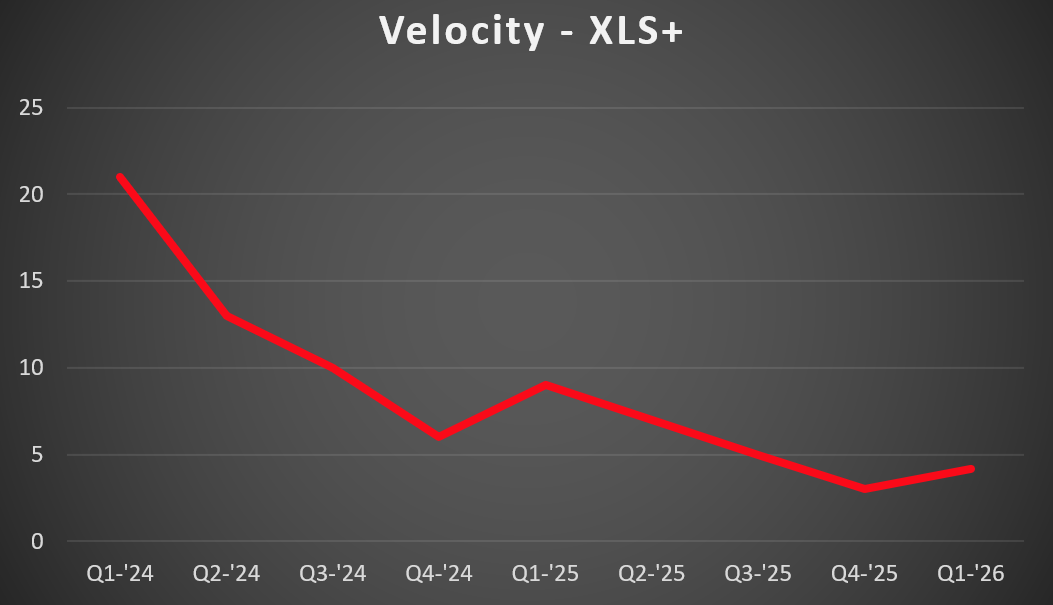

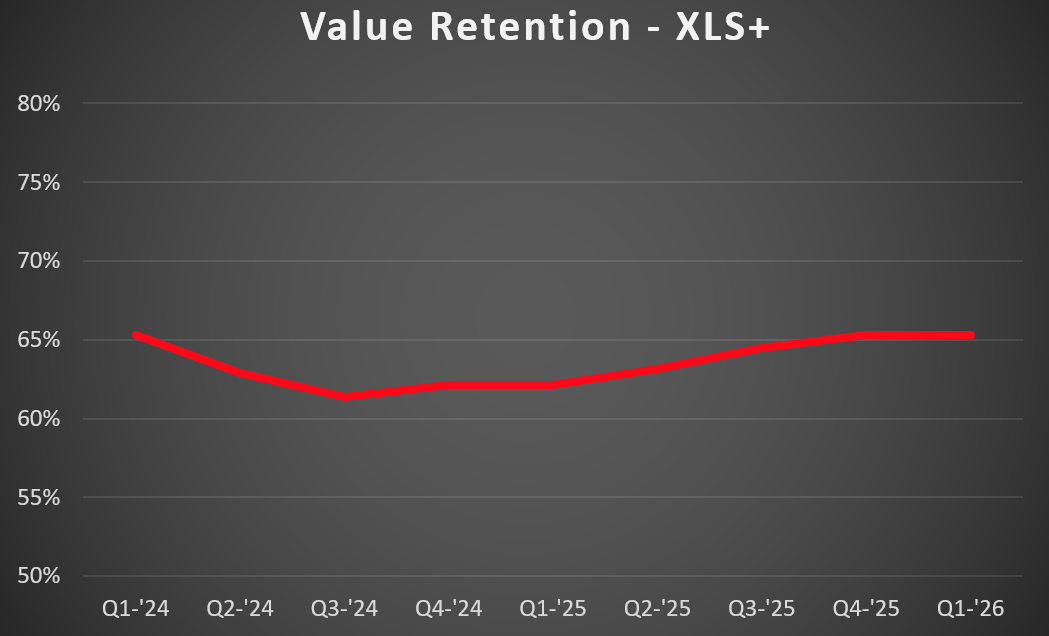

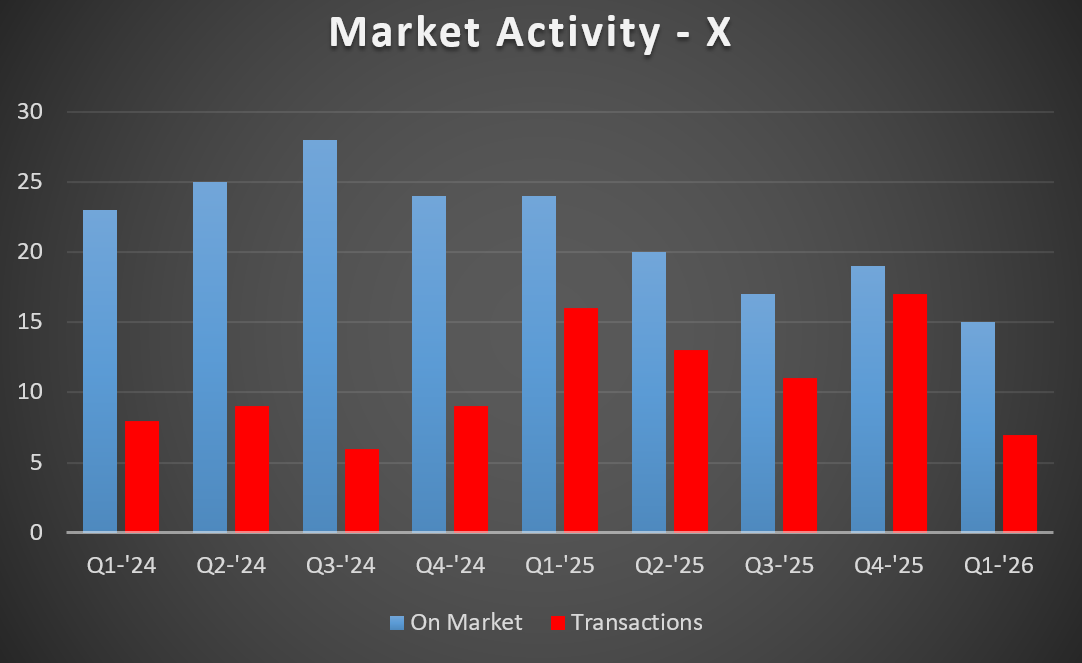

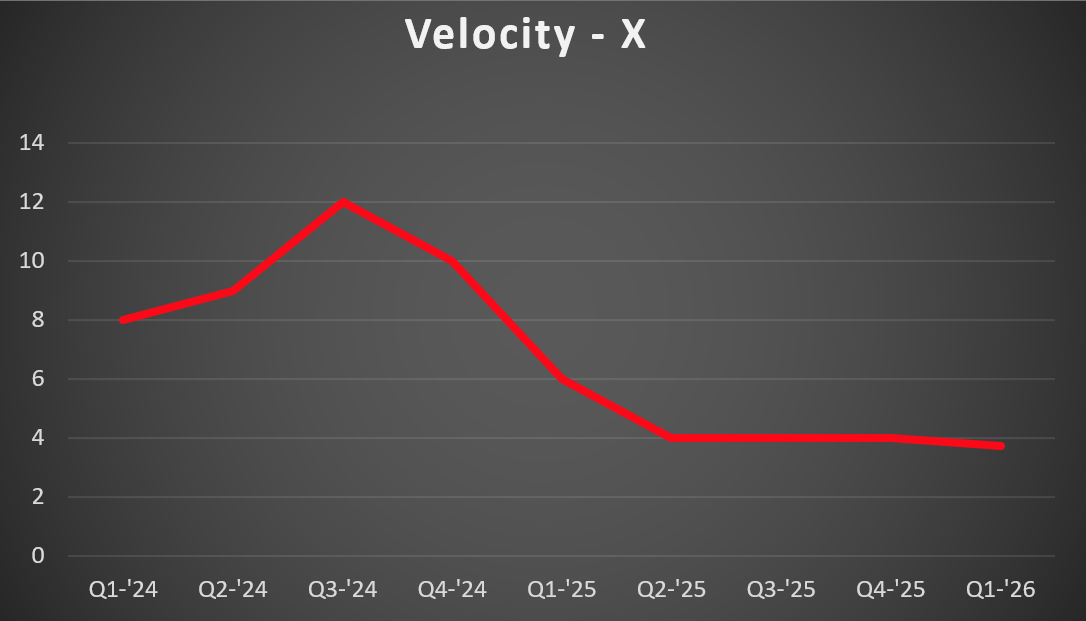

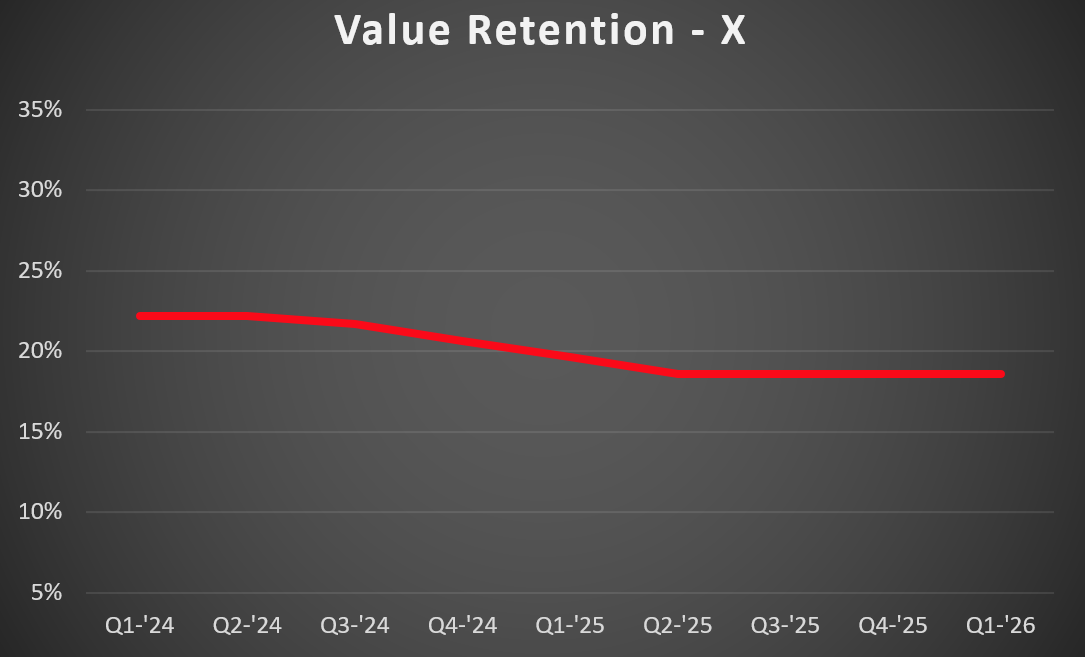

The 900XP inventory has bounced back, and pricing remains stable. There are now 17 listings in this market, after a temporary drop down to 14 during Q4. 9.6% of the active fleet is for sale, but buyers are still struggling to find quality, US-based options. Six aircraft sold during Q1, down slightly from Q4, but a good chunk of the current listings are deal pending. Values are holding steady after increasing during Q4, and buyers continue to pay a premium for late-model, low-time aircraft. With both stable inventory and demand, this market remains balanced for buyers and sellers.