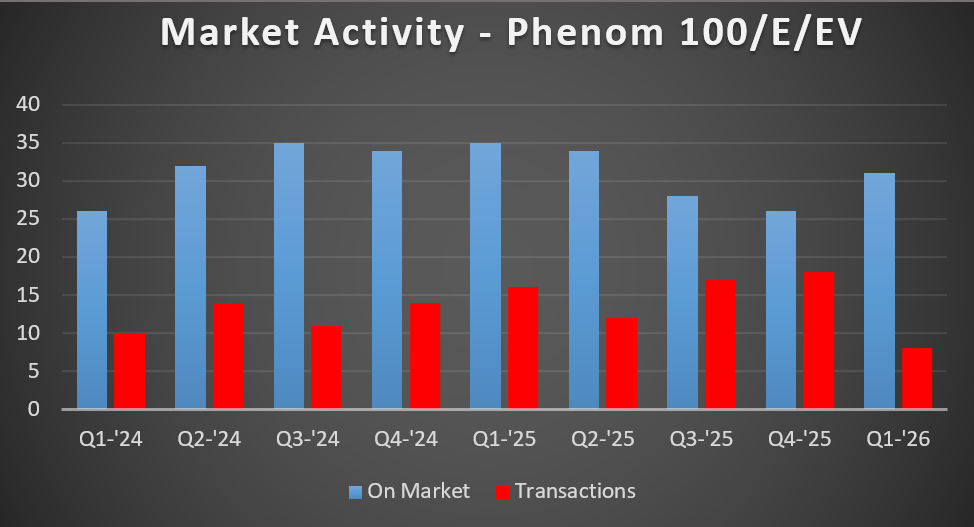

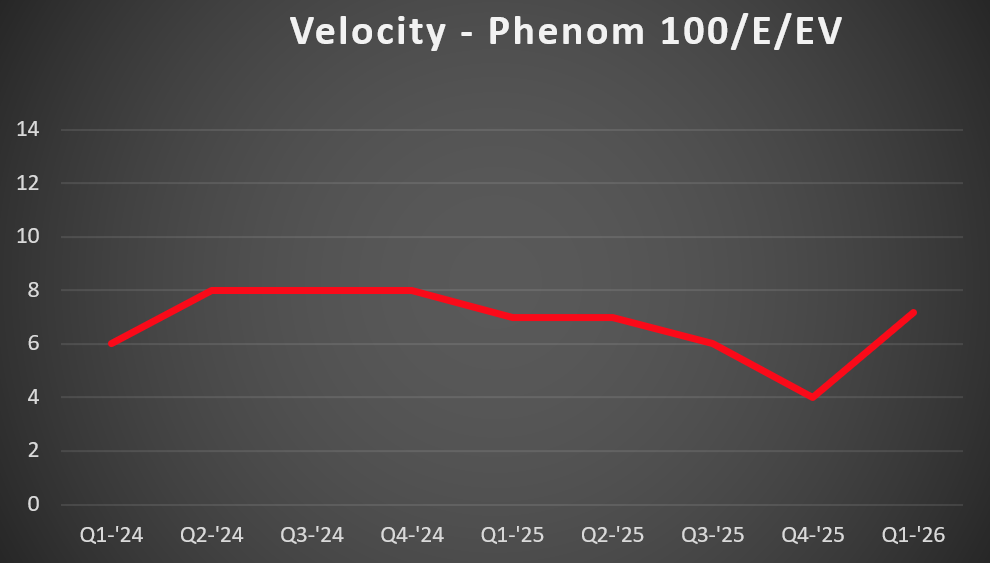

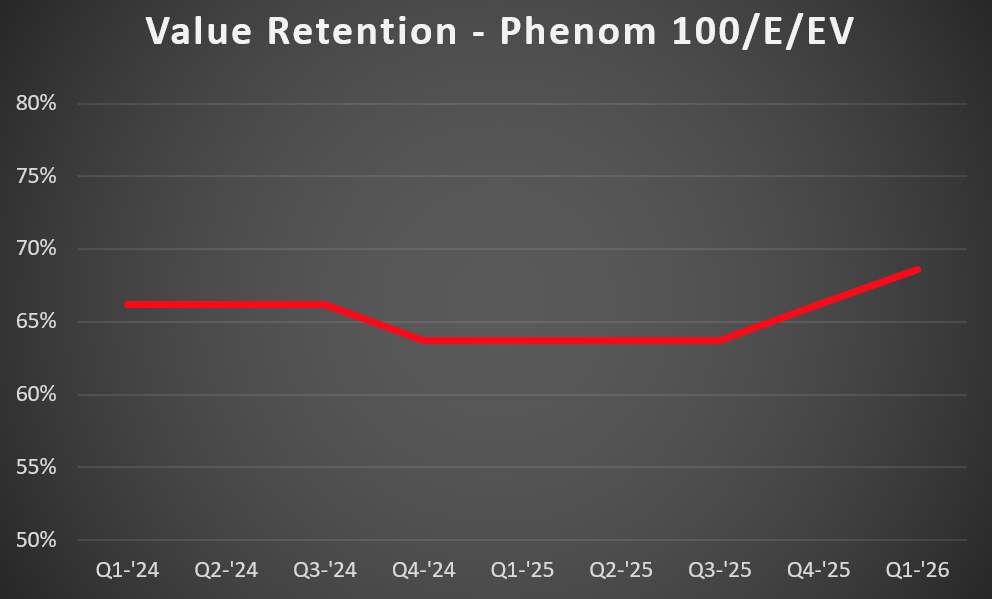

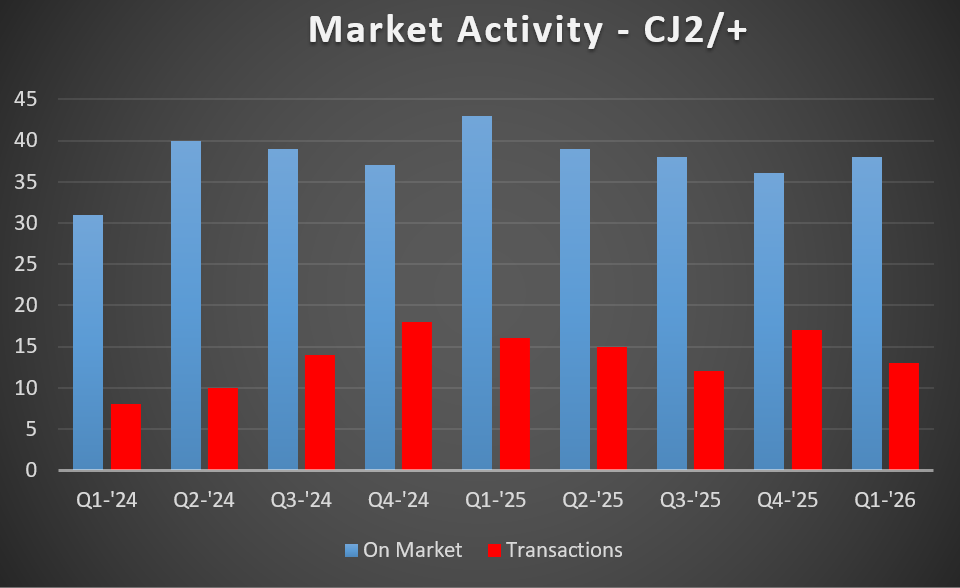

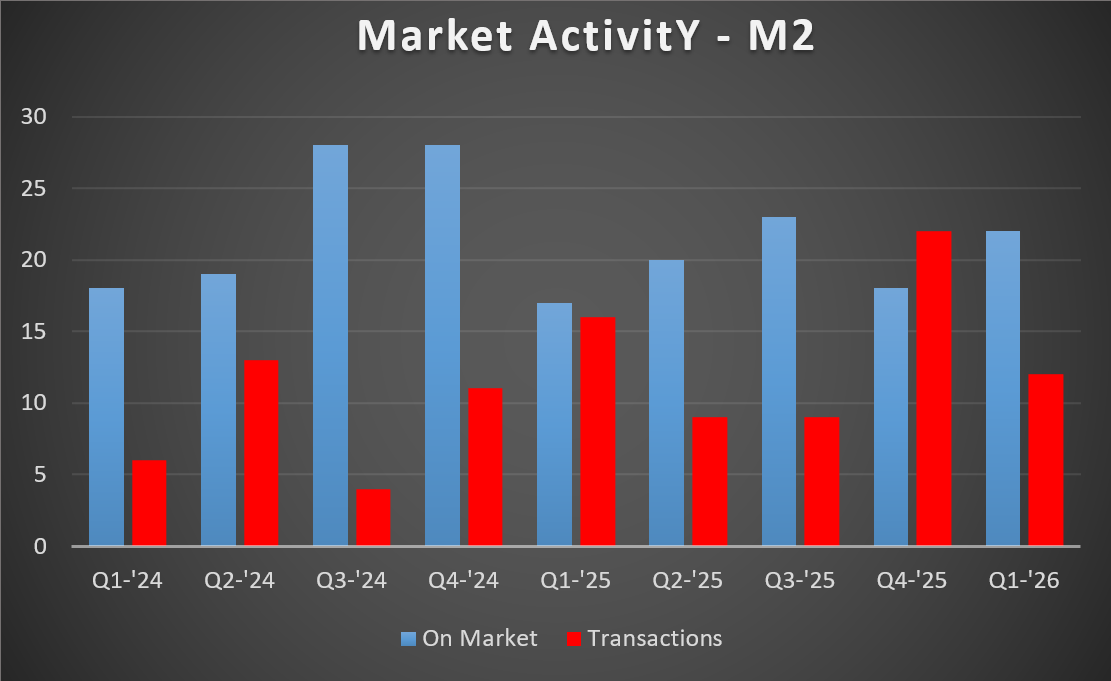

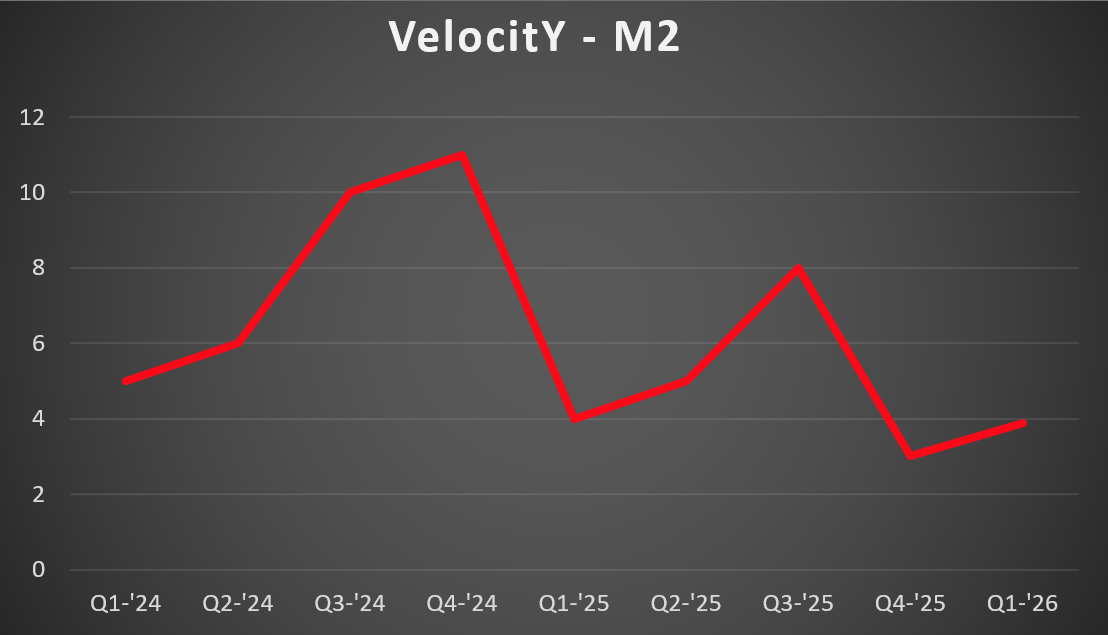

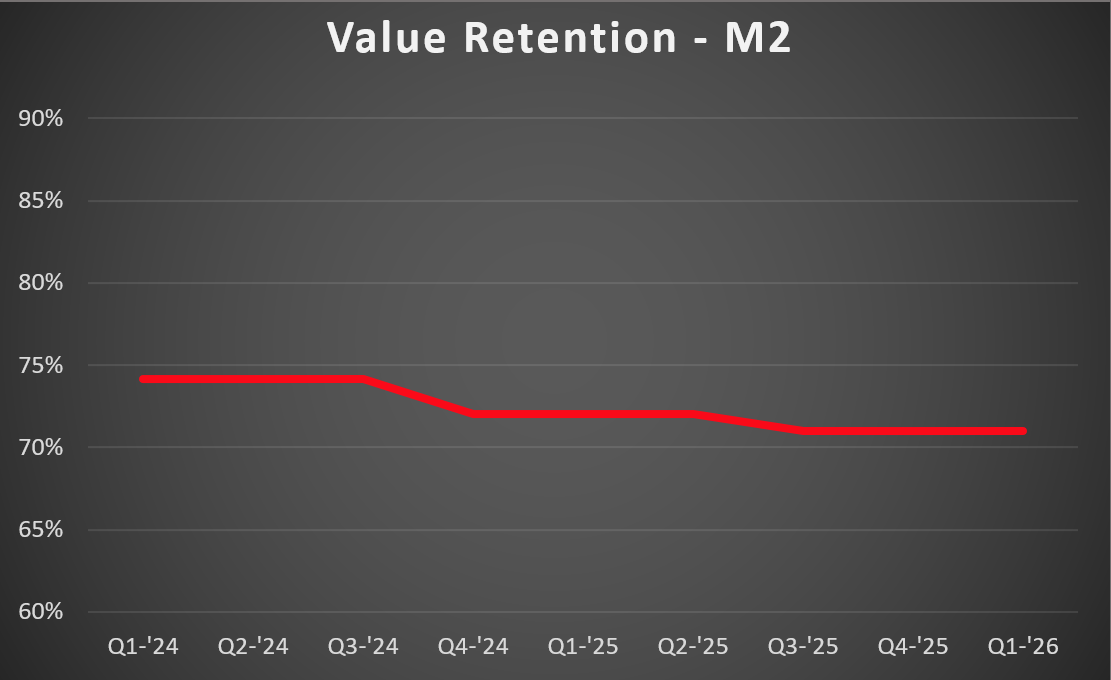

Inventory has bounced back in the Phenom 100 space, but values continue to rise as demand for late-model aircraft remains strong. There are now 31 combined listings between the Phenom 100, 100E and 100EV’s. This is up from 26 last quarter, but still below the 35 listings a year ago. 7.7% of the active fleet is listed for sale, the most since Q2 of 2025. Activity dropped off after a busy Q4, with just eight sales taking place during Q1, the slowest quarter in three years. Even with rising inventory and reduced activity, values climbed during Q1, especially in late model aircraft, where options remain limited. With ample inventory yet strong prices, this market is considered balanced for buyers and sellers.